Authors

- Jocelyn Lee is a Researcher at SACR. She is a dual-degree candidate at Wharton and Penn Engineering, specializing in finance, statistics, and scientific computing. She is an incoming long/short equity analyst at Millennium, with experience across investment banking, fundamental investing, and strategy consulting, and has contributed to research in financial markets. She conducted extensive months of research to develop this study.

Co-author:

- Lawrence Pingree is the Head of Data and AI Security at SACR, where he leads research on data protection, AI security, and agentic security models. He brings more than ten years of analyst experience from Gartner and has authored over 300 research notes across cloud security, endpoint defence, SD-WAN, and AI security.

Executive Summary

The rapid adoption of AI and autonomous agents is not only reshaping enterprise security architectures, it is redefining how security budgets are allocated. As identity, data, and runtime risk converge, a new category: Unified Agentic Defense Platforms (UADP) is emerging as the next major control layer in cybersecurity. While our prior analysis focused on the technical architecture underpinning UADP, this report examines the market through a different lens: how spending is distributed today, which vendors are capturing share, and how platform consolidation will reshape the competitive landscape over the next five years.

The market remains in a transitional phase. Large platform vendors hold disproportionate shares due to their control over identity, cloud, and productivity ecosystems, while the broader landscape is still fragmented across point solutions spanning identity, data, cloud, and AI security. As enterprises rationalize this fragmentation, spending is expected to shift toward integrated platforms that unify identity, data, and behavioral signals, driving a reallocation of market share toward vendors capable of operating a centralized, cross-domain security control plane.

Marketshare and Forecast Findings

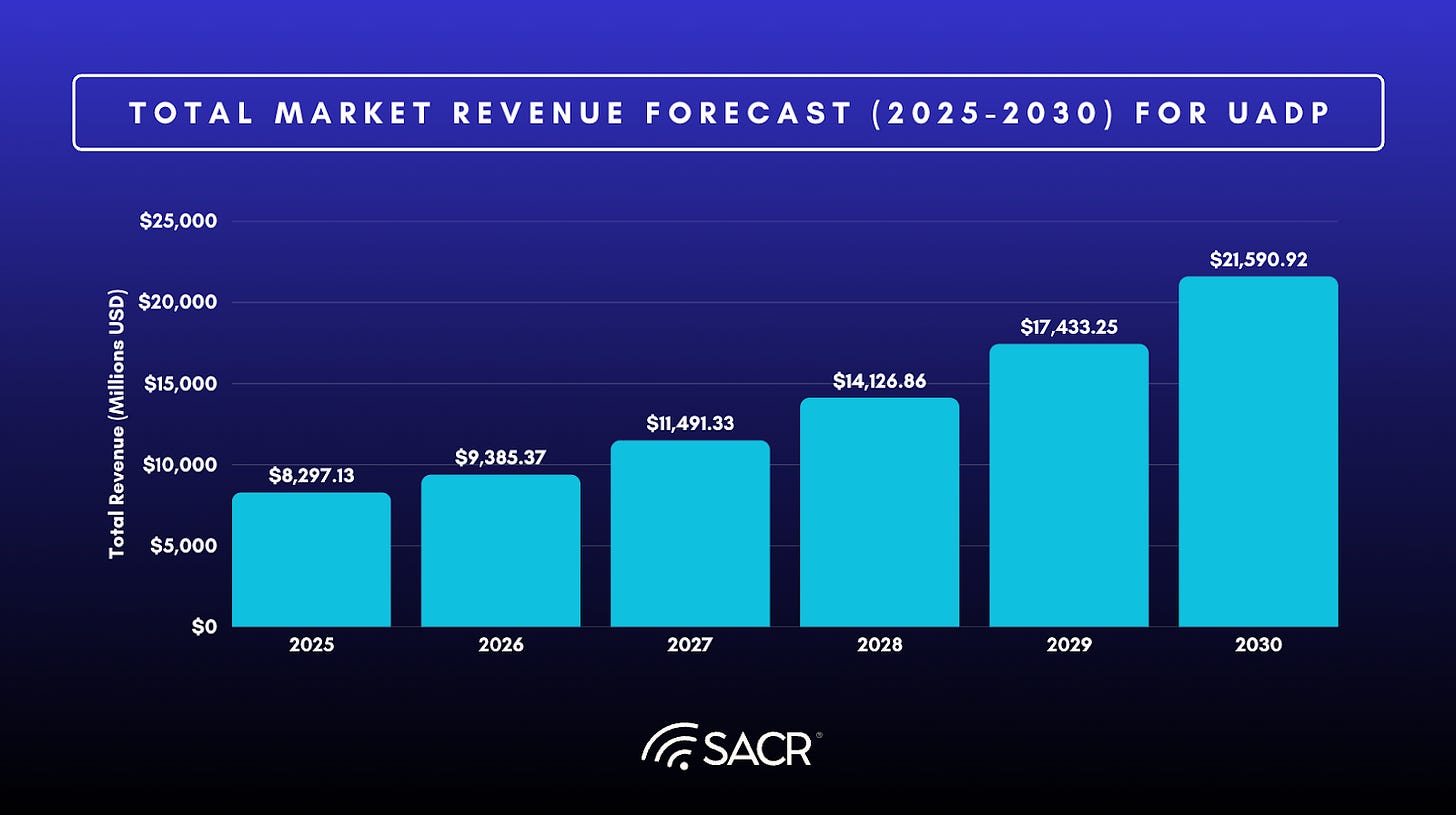

- The UADP market is projected to grow from $8.30B in 2025 to $21.59B in 2030, implying approximately 21.08% CAGR through 2030.

- DLP remains the largest and most mature segment, growing from $3.76 billion to $6.95 billion (13.06% CAGR), anchored by decades of deployment across enterprise environments.

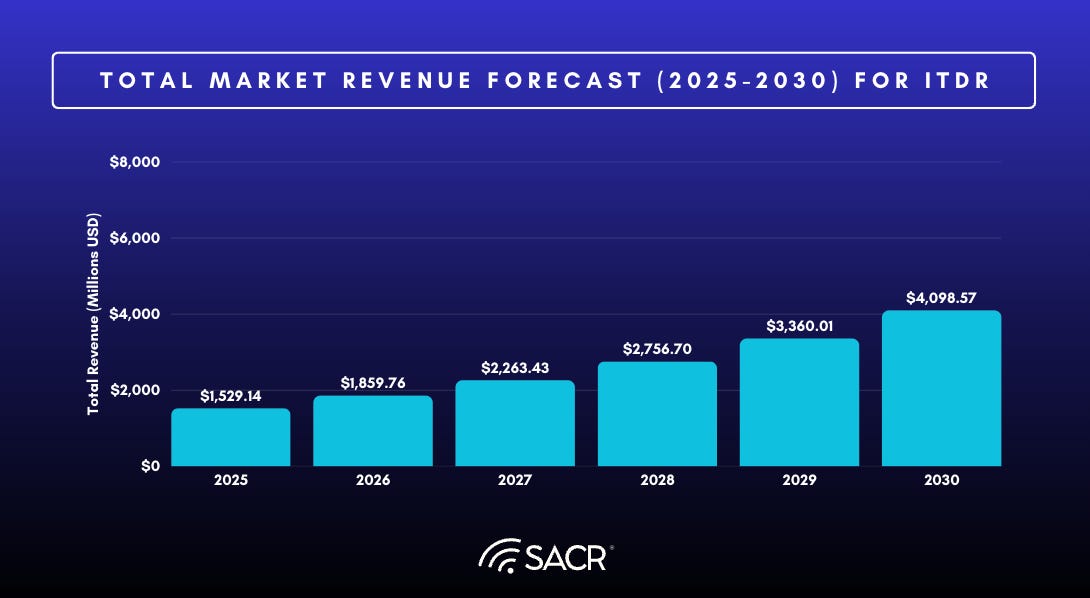

- ITDR is the second largest and second most mature category, expanding from $1.53 billion to $4.10 billion (21.80% CAGR) as identity becomes the primary attack surface.

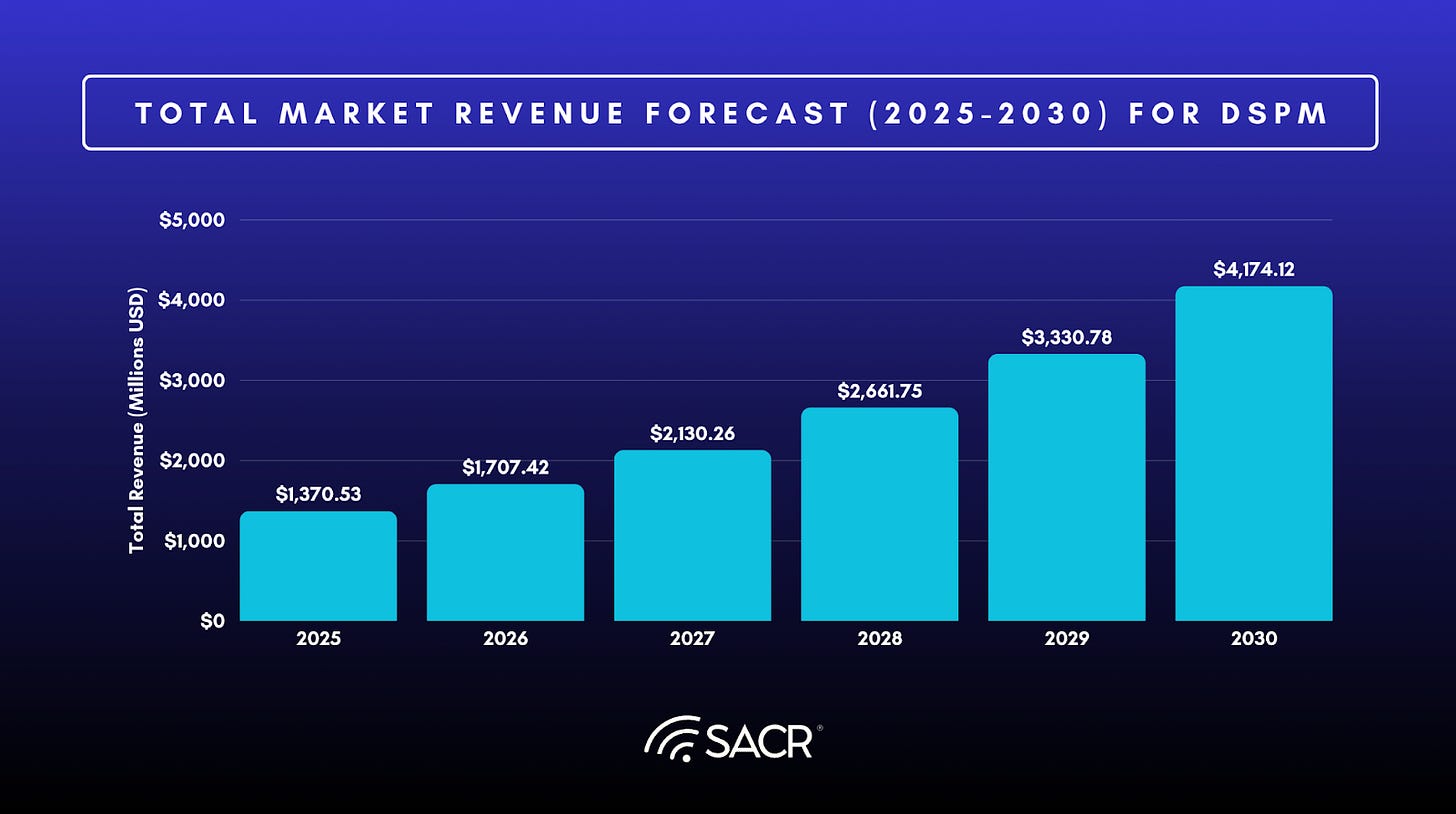

- DSPM scales from $1.37 billion to $4.17 billion (24.95% CAGR) as organizations seek control over sensitive data in cloud and analytics environments.

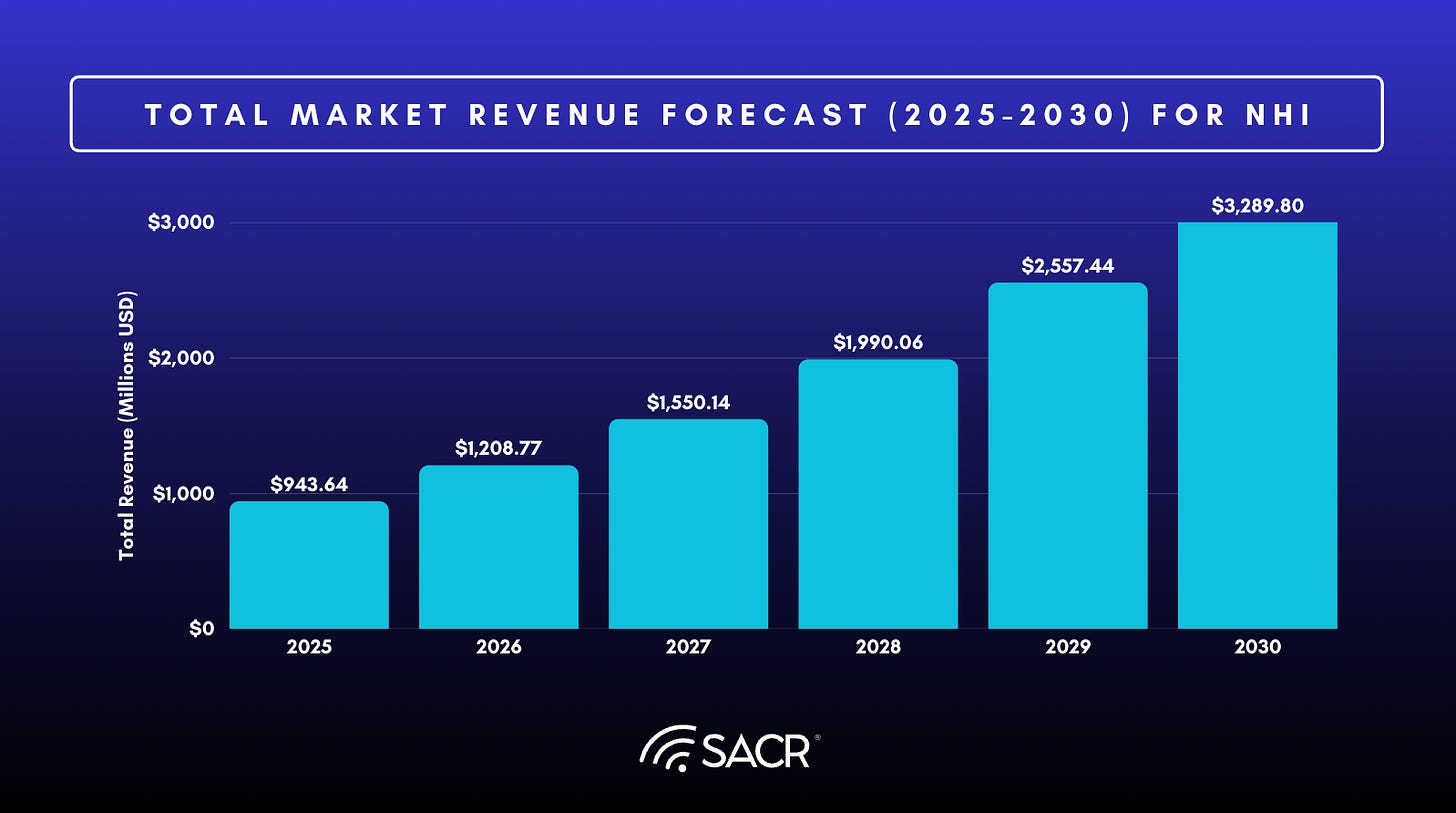

- NHI security expands from $0.94 billion to $3.29 billion (28.37% CAGR) as machine identities proliferate across infrastructure and applications.

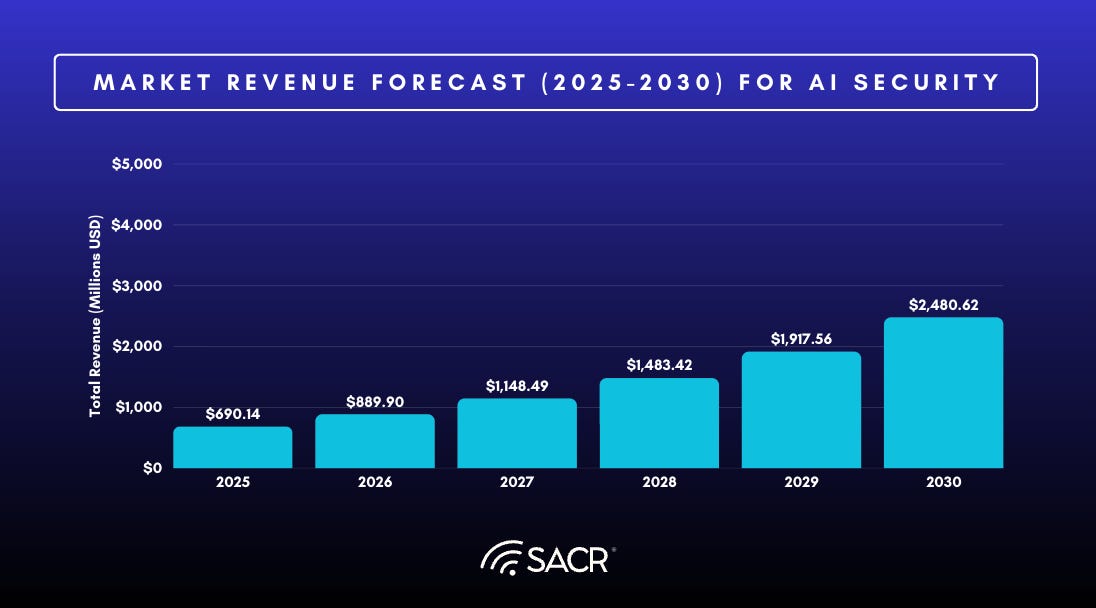

- AI security grows from $0.69 billion to $2.48 billion (29.16% CAGR) as enterprises move AI into production.

Actionable Recommendations

For CiSOs and Practitioners

- Prioritize Unified Control Planes: Shift away from isolated point solutions toward integrated UADP architectures that can correlate signals across domains (data sensitivity, identity privileges, runtime behavior, and AI interactions) in real time.

- Address Runtime Security: Treat AI security as an operational discipline, focusing on controls that monitor and intervene in the runtime layer during live interactions to prevent prompt injection, unauthorized data retrieval, and agent-driven privilege escalation.

- Expand Identity Governance: Extend governance programs to cover the new category of non-human identities, including AI agents and automated workflows, by combining identity visibility, behavioral monitoring, and policy enforcement.

For Vendors

- Pursue Integration: Competitive positioning requires integrating capabilities across the five foundational pillars (DSPM, DLP, NHI, ITDR, and AI security) to assemble a unified operational platform.

- Leverage Distribution and M&A: Platform integration, strategic acquisitions (like Palo Alto Networks acquiring CyberArk, or Google acquiring Wiz), and ecosystem partnerships should be key elements of strategy to capture disproportionate share. Vendors that control identity, cloud, or productivity ecosystems have a strong distribution advantage.

- Focus on AI Runtime: Emphasize capabilities for real-time protection of prompts, model responses, and agent behavior, as this is emerging as the fastest-growing control layer.

For Investors

- Target Intersection Points: Focus on vendors positioned at the intersection of multiple UADP pillars, as they are likely to benefit from platform consolidation dynamics similar to those seen in XDR and CNAPP.

- Identify Acquisition Targets: Anticipate that specialist vendors with differentiated capabilities in high-growth segments (like AI security and NHI governance) will become acquisition targets for larger platforms.

Market Definition

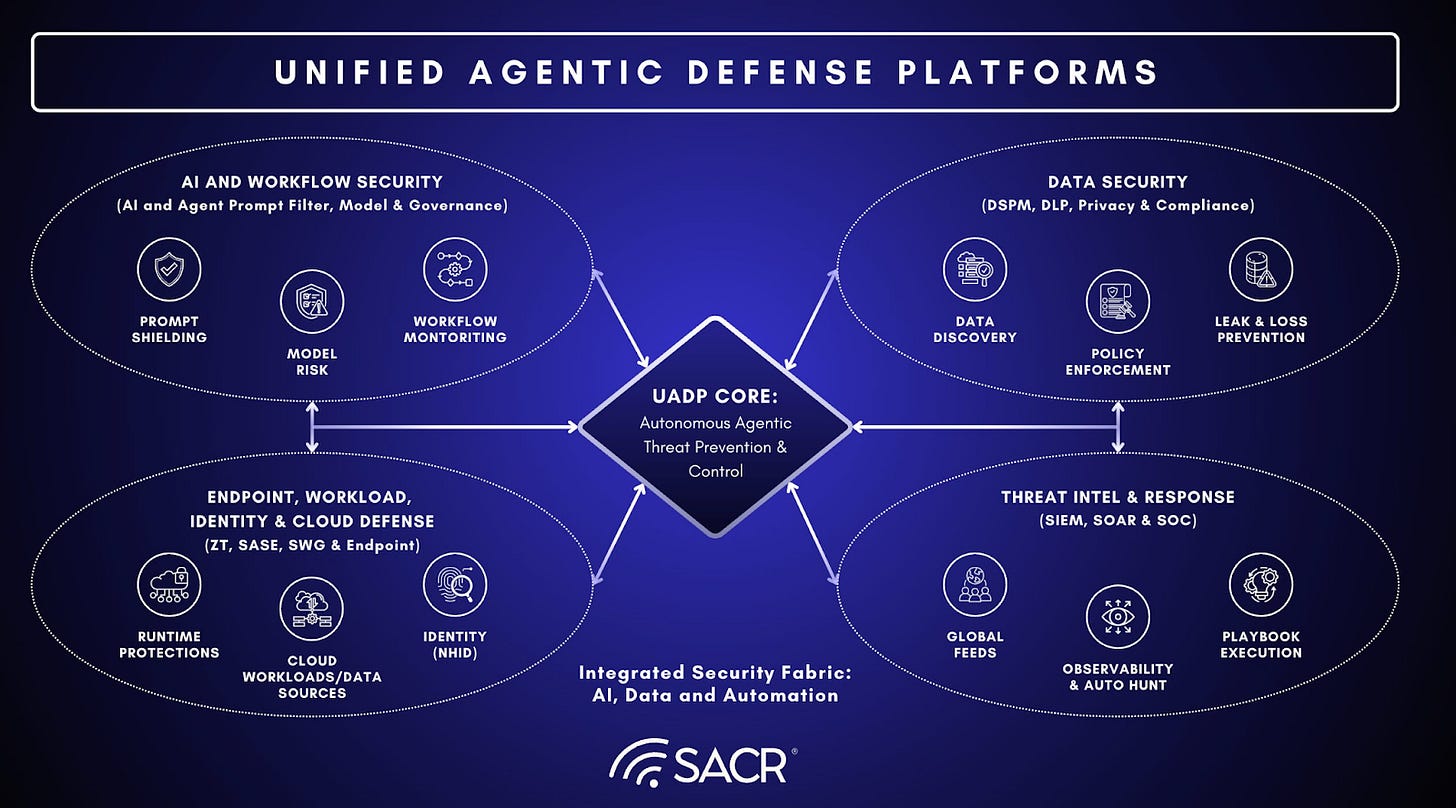

Unified Agentic Defense Platforms (UADP)

This report refers to the emerging architectural category as Unified Agentic Defense Platforms (UADP).

UADPs are Integrated platforms that combine data security, AI and AI agent governance, identity behavior context, runtime enforcement, and detection and response to secure AI models, AI agents, and the data/workflows they process.

Defining Technology, Feature(s), and Service Lines

AI-driven data protection and governance now encompass a comprehensive framework that is specifically designed to address the unique challenges posed by intelligent agents and agentic workflows. This includes advanced capabilities such as classification of sensitive data, redaction or masking of personally identifiable information (PII), and DLP-style inspection and enforcement mechanisms applied directly to prompts, model outputs, and tool calls. The system extends beyond static controls through Data Security Posture Management (DSPM), enabling continuous discovery of sensitive data sources, such as data lakes, cloud-based SaaS applications, vector databases, and RAG stores,and providing contextual risk assessments for these environments. It also detects and monitors Shadow AI, identifying unauthorized or unapproved AI tools, agents, and agentic workflows that operate outside formal governance policies.

UADPs offer AI governance and compliance, which ensures alignment with responsible AI principles and evolving regulatory standards throughout the entire lifecycle of AI pipelines, infrastructure, and workflows. A key component involves identity and intent context,offering visibility into both human and non-human actors (such as agents or service accounts) participating in AI processes, to enable precise policy enforcement decisions. Runtime protection mechanisms provide inline controls at the edge of AI and agent workloads, including through proxies and APIs, enabling real-time intervention when anomalies or violations occur. UADP threat detection and response systems are designed to proactively identify critical risks such as prompt injection or linguistic manipulation (LPCI), agent hijacking, and data tampering, offering automated containment and prevention strategies to safeguard AI system integrity and maintain trust in autonomous workflows.

Introduction and Scope

Report Objective & Methodology

The objective of this report is to estimate the size and growth trajectory of the Unified Agentic Defense Platform market.

The analysis quantifies 2025 market sizes across the five core functional pillars (DSPM, DLP, AI security, ITDR, and non-human identity security) that collectively comprise the UADP architectures, technologies being consolidated, and projects moving forward through 2030 to assess long-term structural growth. For each pillar, the report identifies the top fifteen vendors, estimates the remaining Others segment to capture the long tail of participants, and aggregates the categories to derive a consolidated industry view. Growth is evaluated from both historical momentum as well as forward-looking acceleration.

Estimation Methodology

The UADP market is constructed as a derived consolidation layer on top of the five component pillars rather than an independently sized category. In the base year, UADP is represented as the direct aggregation of the five categories, reflecting a market where capabilities are still purchased separately. From this baseline, the forward model introduces a convergence adjustment that reflects the increasing consolidation of these capabilities into integrated platforms. This adjustment is not applied at the vendor level, but at the market level to capture shifts in enterprise buying behavior, where multiple point solutions are replaced by unified architectures. As a result, while the underlying segments continue to grow independently, the realized UADP market diverges from the simple sum over time.

The methodology for this Industry Outlook Projection employs a structured, triangulated approach using multiple data sources and proprietary estimation models to derive current market share and future growth projections. For publicly traded companies, factual data points such as market share and size are extracted and verified through mandated public disclosures, including SEC filings and official press releases. This analysis also incorporates proprietary and indicative data from market research, funding data, and operational indicators like employee count and hiring patterns. For early-stage startups, revenue is estimated by analyzing funding data, active hiring patterns, and public job postings. Valuation analysis combines pricing and customer count data with valuation-to-revenue multiple disclosures. Estimates are adjusted by consideration of technology emergence, market adoption momentum, replacement lifecycles and overall technology maturity.

The forecast projection incorporates a forward-looking future view analysis based on compound annual growth rate (CAGR) and leverages changes in hiring patterns to gauge company momentum and overall market growth. Revenue is attributed strictly on the basis of functional alignment with the scoped definitions for each pillar. Only monetized software revenue directly mapped to the defined capabilities is included. Where revenue is embedded within broader platform bundles, proportional allocation is applied based on product positioning, disclosure transparency, and competitive context.

Defined Segmentation Method

Each market share estimate presented in this report is paired with a formal market definition to ensure consistency and analytical discipline. Revenue is included only when the capability aligns directly with the defined functional scope of the category. Standalone IAM seat licensing, pure telemetry or SOC analytics platforms, endpoint protection products without integrated data context, backup and recovery solutions, compliance documentation tools, and security services revenue are excluded from the sizing model. This disciplined scoping approach is intended to prevent double counting and to ensure that the resulting estimates reflect architectural convergence rather than simple aggregation of adjacent security markets. This report solely represents Software Analyst Cyber Research (SACR)’s point of view rather than asserts an objective truth.

Core UADP Consolidating Markets

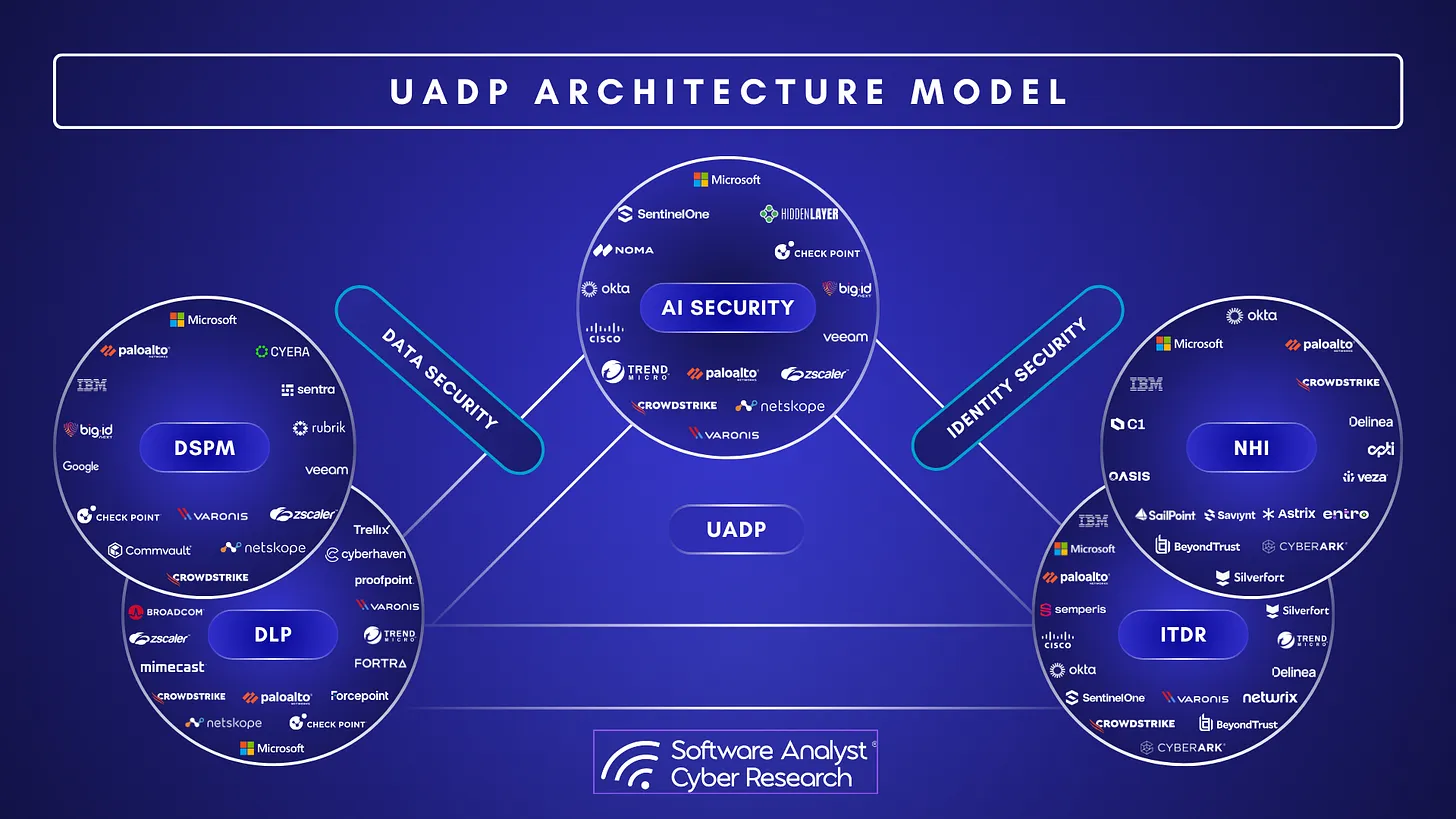

UADPs are constructed from five explicitly defined core categories, each representing a foundational functional pillar with clearly delineated capability requirements used to guide inclusion and analysis.

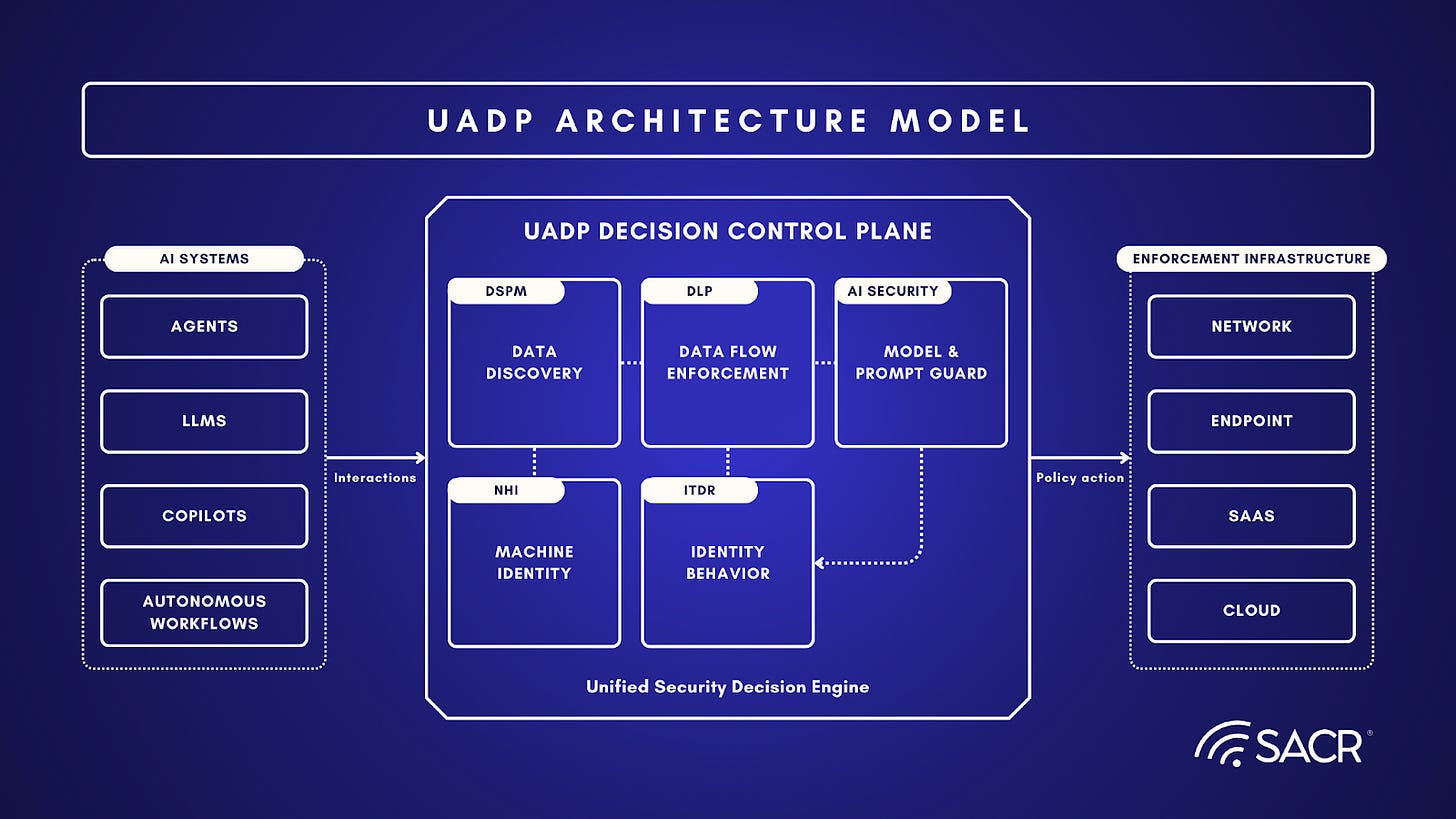

UADP Architecture Model

UADP architectures integrate signals from data security, identity governance, behavioral detection, and AI protection into a unified decision control plane. Policy decisions generated within this layer are enforced through existing infrastructure security controls such as network gateways, endpoint protection platforms, SaaS governance tools, and cloud workload security systems.

Revenue Inclusions and Exclusions

For the purpose of this report, which estimates the size of the UADP market, revenue attribution is strictly limited to integrated platform software aligned with the UADP architectural definition.

The objective of this scoping is to isolate revenue directly associated with unified, cross-domain defense control planes – not adjacent or legacy security categories.

Revenue attributable to UADPs includes monetized software modules that are architecturally integrated and aligned to one or more of the following functional domains within a unified platform: DSPM, DLP, AI Security, NHI, or ITDR.

On the other hand, examples of revenue explicitly excluded from the revenue sizing include:

- Standalone IAM Seat Licensing: Authentication and access management revenue derived from MFA, SSO, directory services, and baseline access control products where no integrated risk reasoning or enforcement control plane exists.

- Pure-Play SIEM, XDR, or SOC Telemetry Platforms: Telemetry ingestion, log analytics, detection platforms, and SOC tooling that lack embedded data context, AI lifecycle governance, and inline enforcement capabilities.

- Endpoint Protection Products (EDR/AV): Endpoint security tools that operate independently of data classification, AI governance, or identity-aware enforcement frameworks.

- Backup, Recovery, and Data Resilience Platforms: Solutions focused on post-breach recovery, archival storage, or resilience rather than live interaction prevention and unified control.

- Pure Compliance Documentation or GRC Platforms: Policy documentation, audit workflow management, and regulatory reporting systems that do not provide runtime intervention capabilities.

- Security Services and Consulting Revenue: Managed services, MSSP contracts, advisory services, professional services, and incident response retainers.

- Standalone Secrets Management or Vaulting:Machine identity tools that do not integrate behavioral detection and data-aware enforcement into a unified reasoning layer.

Sub-Segments Industry Analysis

Historically, capabilities such as data loss prevention, data security posture management, identity threat detection, and machine identity governance developed as separate product categories addressing specific risk surfaces within enterprise environments. However, the increasing interaction between enterprise data, automated identities, and AI-driven workflows is blurring the boundaries between these markets. Vendors are responding by integrating capabilities that were once delivered through standalone tools into broader security platforms capable of providing unified visibility and enforcement across data, identities, and runtime environments.

To understand how this convergence is shaping the emerging Unified Agentic Defense Platform (UADP) market, it is first necessary to examine the underlying markets from which these capabilities originate. The following sections analyze the major security domains that collectively form the foundation of the UADP architecture.

1) Data Loss Prevention (DLP)

DLP in the UADP market is a security capability that monitors and enforces policies on data in motion and use, preventing sensitive information from being exposed or exfiltrated through real-time inspection, detection, and blocking mechanisms across systems and workflows.

The DLP market is projected to grow from $3.76B in 2025 to $6.95B in 2030, implying a ~13.06% CAGR.

2025 Market Share Analysis

The current structure of the DLP market reflects a fundamental shift in how enterprise data is created, accessed, and transmitted. Historically, DLP deployments were concentrated at network gateways and managed endpoints, where traffic inspection and perimeter enforcement were feasible. However, as enterprise workflows have moved toward SaaS applications, cloud collaboration platforms, and browser-mediated interactions, DLP deployment models have evolved accordingly. As a result, market share is increasingly determined not solely by inspection capabilities or classification depth, but by control over the operational surfaces where data flows. Vendors that are embedded within collaboration environments, SaaS ecosystems, and access layers are better positioned to apply data protection policies with minimal deployment overhead. This shift has reoriented competitive dynamics away from standalone inspection engines and toward distribution advantage within existing enterprise workflows.

Top 15 Players in 2025

Platform distribution advantages

A significant portion of market share is concentrated among vendors that operate platforms where enterprise data already resides. Productivity suites, cloud collaboration environments, and integrated compliance frameworks provide natural insertion points for DLP controls. Within these environments, data protection capabilities are often activated through policy configuration rather than deployed as separate products. Microsoft is a primary example of this dynamic. Its DLP capabilities are integrated across Microsoft 365, Purview, and related compliance services, enabling organizations to extend data protection policies across email, documents, and collaboration workflows without additional infrastructure. More broadly, platform vendors benefit from pre-existing integration into day-to-day enterprise operations, which lowers friction for adoption and accelerates deployment at scale.

This distribution advantage is further reinforced by the increasing integration of AI capabilities into productivity environments. As generative AI systems interact directly with enterprise content, data protection is increasingly treated as a prerequisite for safe AI adoption. Vendors that control document repositories and collaboration layers can extend existing classification and governance frameworks into AI-driven workflows with limited incremental effort. Over time, this dynamic supports a consolidation trend characterized by a “good enough, already licensed” adoption pattern. Enterprises with established governance and compliance programs often expand existing platform-native DLP capabilities rather than procure standalone solutions. Consequently, a meaningful portion of incremental DLP adoption is driven by expansion within installed platforms rather than net-new product deployments.

SSE and SASE platform expansion

A second driver of market evolution is the growing role of SSE and SASE platforms in delivering DLP capabilities at the traffic layer. As enterprise data increasingly moves across SaaS applications, web sessions, and unmanaged devices, enforcement is shifting toward inline control points rather than traditional endpoint or gateway-based architectures. These platforms embed DLP directly into secure web gateways, CASB layers, and browser-mediated access, enabling real-time inspection and policy enforcement at the point of data interaction. This positioning is particularly effective in cloud-first environments where data flows bypass traditional network controls. Recent M&A activity reinforces this shift toward access-layer DLP with improved data context. Zscaler’s acquisition of Avalor enhances policy accuracy through deeper classification and context, while Netskope’s acquisition of Dasera expands visibility into structured data environments, strengthening enforcement across SaaS and cloud data flows. Palo Alto Networks’ acquisition of Talon Cyber Security further extends DLP enforcement into the enterprise browser, enabling policy control directly within user sessions.Collectively, these developments indicate that SSE and SASE vendors are redefining DLP as an inline, access-layer capability, positioning them to capture a growing share of net-new deployments in distributed, SaaS-driven environments

Pressure on legacy gateway DLP vendors

Vendors historically associated with gateway centric DLP architectures face slower incremental growth. Many of these platforms were designed around inspecting traffic moving through corporate networks and enforcing policies through tightly controlled endpoints guarded by centralized networks and entrances to the internet . While these architectures remain deeply embedded within large enterprises, they are less aligned with cloud native and SaaS aligned environments where data moves directly between Cloud and SaaS applications or across browser based collaboration applications and tooling.

This does not imply immediate displacement. Vendors such as Broadcom continue to maintain a substantial installed base in endpoint DLP, supported by mature classification engines and highly granular policy frameworks developed over many years of enterprise deployments. However, the pace of new deployments increasingly favors architectures that require fewer infrastructure or endpoint dependencies and integrate more naturally with SaaS and cloud collaboration environments. As a result, legacy vendors are likely to retain meaningful market share but capture a smaller portion of net new growth and are increasingly being displaced by vendors with better alignment with SaaS, Browser and Cloud native data loss prevention functionality.

2) Data Security Posture Management (DSPM)

DSPM in the UADP market is a security capability that discovers, classifies, and monitors sensitive data across environments, identifying exposure risks and misconfigurations through continuous visibility into data location, access paths, and contextual usage.

The DSPM market is projected to grow from $1.37B in 2025 to $4.17B in 2030, implying a ~24.95% CAGR.

2025 Market Share Analysis

The current distribution of share reflects both where enterprise data resides and which teams are responsible for governing it. Unlike earlier data security tools focused on classification or compliance reporting, DSPM emerged to address a visibility gap created by rapid cloud adoption. Sensitive data is now distributed across object storage, SaaS platforms, analytics environments, and AI pipelines that traditional controls were not designed to monitor. As a result, DSPM adoption is driven by multiple enterprise buying centers, producing a fragmented market in which vendors gain traction through distinct operational entry points.

Top 15 Players in 2025

Data governance heritage and entitlement visibility

One of the largest problem spaces in enterprise environments has been data visibility. Thus, several of the foundational leaders in DSPM gained share by building deep visibility into enterprise data estates and the identities that can access them. Vendors that originated in data governance or insider risk detection developed strong capabilities around entitlement mapping, classification depth, and remediation workflows. These features remain particularly valuable in environments where sensitive data resides in collaboration platforms, file systems, and enterprise SaaS applications.

Varonis illustrates this dynamic. Its long focus on entitlement analysis and automated remediation positioned it well as organizations began seeking ways to understand which users and services could access sensitive information stored across large collaboration environments. In many enterprises, DSPM adoption initially occurs through governance teams attempting to reduce overexposed data stores or enforce least privilege access policies. Vendors that built mature discovery engines and remediation automation therefore retain strong positions in environments where operational data governance remains the primary objective.

Cloud security platforms expanding into data visibility

A second channel for DSPM adoption has emerged from cloud security and CNAPP platforms. As organizations migrated infrastructure and analytics workloads into public cloud environments, cloud security teams began seeking ways to identify sensitive data residing inside cloud storage, databases, and data pipelines. In these environments, DSPM capabilities are often purchased as an extension of broader cloud security and risk management programs.

Vendors such as Wiz and Palo Alto Networks have benefited from this shift by embedding data discovery and exposure mapping inside their existing cloud security platforms. When organizations already rely on a cloud security graph to monitor misconfigurations and workload vulnerabilities, adding visibility into sensitive data stores becomes a natural adjacency. This dynamic has allowed cloud security platforms to expand into the DSPM category without necessarily positioning it as a standalone product. Instead, DSPM capabilities function as an additional layer of context within broader cloud risk management frameworks.

Cyber resilience platforms entering the category

Another emerging source of DSPM adoption comes from cyber resilience and backup vendors expanding beyond traditional recovery capabilities. Historically, backup platforms focused on ensuring that organizations could restore systems after ransomware incidents. However, as ransomware attacks increasingly target sensitive data repositories, resilience programs have begun incorporating preventative visibility into data exposure.

Vendors such as Rubrik and Veeam have therefore expanded their platforms to include capabilities that identify where sensitive data resides and how it is accessed before an incident occurs. This evolution reflects a broader shift in enterprise security priorities. Organizations are no longer evaluating data protection solely through the lens of recovery performance but also through their ability to understand and reduce data risk before an attack takes place. As a result, DSPM spending is increasingly appearing within cyber resilience budgets rather than purely within governance or compliance programs.

Platform bundling and distribution advantages

As the category matures, distribution and platform leverage are becoming more important determinants of market share than discovery technology alone. Many enterprises now view DSPM as a prerequisite for broader initiatives such as AI governance, data access control, or regulatory compliance. When DSPM is bundled within larger security or compliance suites, adoption can scale quickly through attached sales and expansion rather than through dedicated procurement cycles.

Large platform vendors therefore benefit from significant distribution advantages. When DSPM capabilities are embedded within cloud security, compliance platforms, or data governance frameworks, organizations can activate sensitive data visibility without deploying a separate tool. This dynamic has allowed vendors with large installed bases to expand DSPM adoption across existing customers even if their products are not the deepest in every feature category. At the same time, specialized DSPM vendors remain competitive when buyers prioritize deep classification, granular entitlement mapping, and operational remediation.

3) AI Security

AI security in the UADP market is a security capability that monitors and protects AI systems and workflows, preventing misuse, data leakage, and model abuse through real-time inspection, policy enforcement, and control of prompts, outputs, and agent behavior.

The AI Security market is projected to grow from $0.69B in 2025 to $2.48B in 2030, implying a ~29.16% CAGR.

2025 Market Share Analysis

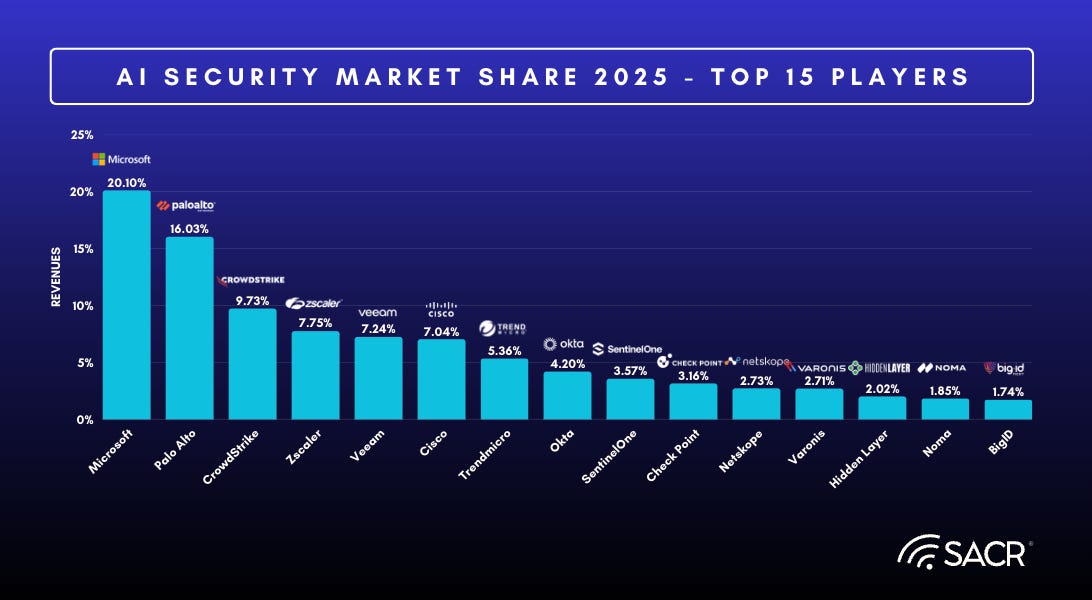

The current distribution of share reflects a category that is still forming, with adoption largely occurring through extensions of existing security and cloud platforms rather than standalone procurement. As enterprises deploy AI within established infrastructure and productivity environments, security controls are frequently embedded into broader platforms, resulting in early share concentration among large ecosystem vendors.

At the same time, a fragmented set of vendors continues to compete across specific segments of the problem, including runtime protection, AI governance, and data-centric controls. Vendors such as Palo Alto Networks, CrowdStrike, Zscaler, Check Point, Netskope, Varonis, HiddenLayer, Noma, and BigID represent a mix of platform extensions and emerging AI-focused capabilities, illustrating a market where platform distribution and point-solution depth coexist.

Top 15 Players in 2025

Platform vendors benefit from control of the surrounding ecosystem

A significant share of AI security adoption is accruing to vendors that control the environments where AI systems are built and consumed. Cloud platforms, productivity suites, and identity layers provide natural insertion points for AI security controls, allowing vendors to extend governance and enforcement into AI workflows with minimal deployment friction.

Microsoft’s position reflects this dynamic. Its share is driven not only by discrete AI security features, but by its ability to integrate controls across Entra, Purview, Defender, and Microsoft 365. This enables organizations to address AI-related risks within existing compliance and security programs rather than through separate product adoption. More broadly, platform control is emerging as a primary determinant of share, as enterprises favor solutions that inherit existing identity, data, and policy context.

Runtime protection is emerging as the fastest growing control layer

As AI deployments move from experimentation into production, security priorities are shifting toward runtime enforcement. Early investment focused on governance and model visibility, but the most critical risks such as prompt injection, unauthorized data access, and unsafe agent behavior occur during live interactions.

This shift is driving demand for inline controls that operate within AI workflows. Vendors such as Check Point, SentinelOne, and Netskope are incorporating capabilities to inspect prompts, govern agent actions, and enforce policies in real time. Check Point’s acquisition of Lakera reflects this transition toward runtime-centric security, emphasizing protection at the interaction layer rather than static model analysis. As enterprises operationalize AI systems, runtime protection is likely to capture a growing share of spending.

AI security is increasingly being pulled into data security and cloud security budgets

Although AI security is often discussed as a standalone market, much of its actual budget is being pulled through adjacent categories and the platform concept articulated as UADP. In many enterprises, the first concrete AI security question is not how to secure a model in the abstract, but how to prevent sensitive enterprise data from being exposed through prompts, retrieval systems, or agentic workflows. In other environments, the starting point is cloud security, where teams need visibility into which models, datasets, and AI services are running in production and how they connect to broader infrastructure.

This creates a market structure in which AI security adoption frequently rides on top of existing data security and cloud security programs. Data-centric vendors such as Varonis and BigID address AI risk through classification, access governance, and visibility into how sensitive data is accessed by AI systems. In parallel, cloud and access-layer vendors such as Palo Alto Networks, Zscaler, and Netskope incorporate AI visibility and controls into broader infrastructure and traffic management frameworks. This results in a market structure where AI security adoption is pulled through existing control planes, rather than driven by standalone purchasing decisions. Over time, vendors that can embed AI security within broader platforms, aligned to UADP, are likely to benefit from this dynamic.

Specialists retain an advantage where workflow depth matters most

Despite the distribution advantages of large platforms, specialist vendors remain highly relevant because product differentiation in AI security is still real. The category is evolving quickly, and many enterprises require controls that go beyond broad platform visibility. This is particularly true in environments where organizations are building their own AI applications, orchestrating agents, or securing complex RAG and MCP-based workflows. In these use cases, buyers often prioritize technical depth, response latency, and workflow-level interpretability over broad suite integration.

Vendors such as HiddenLayer and Noma focus on AI-native protections, including model behavior monitoring, prompt inspection, and runtime defenses tailored to AI systems. These capabilities are particularly relevant in high-maturity environments where buyers prioritize low-latency enforcement, fine-grained control, and interpretability of AI interactions. That type of depth remains valuable because many broader platforms still have uneven coverage across agent-to-agent interactions, tool authorization, and runtime context analysis. As a result, specialists are likely to retain share in high-maturity AI environments even as broader platforms absorb more baseline category demand.

4) Non-human Identities (NHI)

Non-human identity (NHI) security in the UADP market is a security capability that manages and protects machine identities, preventing unauthorized access and credential misuse through continuous visibility, governance, and enforcement across service accounts, APIs, and automated workloads.

The NHI market is projected to grow from $0.94B in 2025 to $3.29B in 2030, implying a ~28.37% CAGR.

2025 Market Share Analysis

The current distribution of share in the NHI market reflects the fact that machine identity security has evolved beyond a narrow infrastructure concern into a core operational control layer. Service accounts, API keys, certificates, workload identities, and increasingly AI-driven processes act as the primary mechanism through which enterprise systems access data and execute workflows. As a result, the category is being shaped by multiple overlapping buying motions, including privileged access management, cloud IAM, secrets management, and identity governance. This has produced a market structure in which identity incumbents, cloud platform providers, and emerging specialists all retain meaningful positions, with share distributed according to where identity control and enforcement already exist within enterprise environments.

Top 15 Players in 2025

Identity incumbents benefit from policy authority and installed trust

A meaningful portion of NHI share continues to accrue to vendors that already own identity governance and privileged access decisions inside large enterprises. In many organizations, the first response to machine identity sprawl is not to create a new budget category, but to extend existing identity and access governance frameworks to cover service accounts, credentials, and privileged non-human access. Vendors that already control entitlement policy, vaulting, or privileged access workflows therefore benefit from a significant distribution advantage.

CyberArk illustrates this dynamic. Its position in the market is strengthened not simply by machine identity discovery on its own, but by its role as a trusted control point for privileged access and secrets management across enterprise environments. That becomes more important as organizations seek to govern not only which credentials exist, but also which automated identities can reach sensitive systems and under what conditions. The broader implication is that incumbent identity vendors retain an important share advantage where buyers view NHI as an extension of privileged access control rather than as a greenfield cloud security purchase.

AI agents are expanding the category beyond traditional machine identities

A key factor contributing to the continued evolution of the category is the expansion of automated and AI-driven workflows, which are broadening the definition of what constitutes a non-human identity. Traditional NHI programs focused on static credentials such as secrets, keys, and service accounts. However, modern systems increasingly rely on automated processes that retrieve data, invoke APIs, and execute tasks across distributed environments. This shift increases demand for platforms that can connect identity governance to data access, workflow context, and execution behavior. Vendors such as Palo Alto Networks, CrowdStrike, and Okta are extending identity and security capabilities to address these more dynamic forms of non-human access, particularly in environments where identity signals must be evaluated alongside runtime activity. As automated systems become more deeply integrated into enterprise workflows, NHI share is likely to shift toward vendors capable of governing both static credentials and dynamic access relationships, particularly where identity intersects with data access and operational execution.

Platform vendors are absorbing NHI into broader security architectures

As with DSPM and AI security, the NHI category is increasingly being absorbed into larger security platforms. Many enterprises do not want machine identity security to operate as an isolated control plane disconnected from data protection, runtime monitoring, and cloud security telemetry. Instead, they want identity context to inform broader enforcement decisions across the stack. This is especially true in environments where automated systems are retrieving sensitive data or performing actions inside production workflows.

Large platform vendors therefore benefit when NHI can be positioned as part of a broader architecture rather than as a standalone control. Palo Alto Networks’ acquisition of CyberArk is important in this regard because it signals that identity security, including non-human identity control, is becoming a core layer within larger security fabrics rather than remaining confined to specialist identity vendors. The same pattern is visible more broadly across the market as platforms attempt to unify identity signals with runtime and data context. Over time, this should support share gains for vendors that can embed NHI into broader operational security workflows rather than treat it as a separate vaulting or governance tool.

5) Identity Threat Detection & Response (ITDR)

The ITDR market is projected to grow from $1.53B in 2025 to $4.10B in 2030, implying a ~21.80% CAGR.

2025 Market Share Analysis

The current distribution of share in the ITDR market reflects a category that is expanding rapidly as identity has evolved from a simple authentication layer into a live attack surface. As attackers increasingly target sessions, tokens, delegated privileges, and identity control planes rather than only endpoints or network perimeters, enterprises are rethinking identity security as a detection and response problem rather than solely a governance problem. Large ecosystem vendors hold a disproportionately large share because identity telemetry is deeply embedded within broader identity, endpoint, and cloud security platforms. As organizations extend identity controls across SaaS applications, cloud workloads, and hybrid infrastructure, many detection and response capabilities are purchased as extensions of existing ecosystems rather than as standalone identity security tools. The market’s two dominant players – Microsoft and Crowdstrike – together account for more than half of total ITDR revenue, reflecting the structural advantage of vendors that already sit at the identity and endpoint control plane across enterprise environments.

Top 15 Players in 2025

Identity control points create a structural distribution advantage

A meaningful portion of ITDR share continues to accrue to vendors that already sit at the identity control plane. In many enterprises, the fastest path to ITDR adoption is to extend existing identity infrastructure with behavioral monitoring, anomalous access detection, and response workflows. Vendors that already manage authentication, conditional access, privilege assignment, and session policies therefore have a natural advantage because they can place detection and enforcement close to the source of identity risk.

Microsoft illustrates this dynamic. Its position in ITDR is supported not only by threat detection capabilities, but by the fact that Entra, Defender, and the broader Microsoft security stack already operate at the intersection of identity, endpoint, and access policy. This gives Microsoft a strong distribution channel for identity-centric detection and automated response, particularly in organizations that already rely on its identity infrastructure. More broadly, the market implication is that vendors controlling authentication and access policy are well positioned to absorb ITDR into broader identity operations rather than leave it as a standalone category.

Endpoint and XDR vendors are pulling ITDR into broader detection platforms

A second force shaping market share is the growing role of extended detection and response platforms in identity threat detection. Many real-world identity attacks do not occur in isolation — token theft, session hijacking, privilege escalation, and lateral movement often intersect with endpoint compromise, cloud control plane abuse, or suspicious network behavior. As a result, many buyers increasingly prefer identity threat detection capabilities integrated into a wider detection and response platform rather than operated as a separate identity-only workflow.

This dynamic favors vendors that can correlate identity signals with endpoint, cloud, and threat intelligence telemetry. CrowdStrike’s 18.08% share reflects this motion directly — its identity protection product has been reinforced by the platform’s endpoint and cloud telemetry, giving buyers a unified view of identity and endpoint risk within a single investigation workflow. SentinelOne follows a similar trajectory, having expanded from endpoint-centric visibility toward a broader detection fabric that includes identity signals. In practice, ITDR often enters the enterprise through SOC modernization and platform consolidation rather than through a standalone identity security purchase, which should support continued share gains for vendors that position identity threat detection as part of a unified investigation and response workflow.

Active Directory remains the primary attack surface driving specialist share

A distinct and structurally important segment of ITDR share accrues to vendors focused specifically on Active Directory and Entra ID threat detection. The ITDR category emerged in direct response to the proliferation of directory-targeting attacks, including credential theft techniques, lateral movement through directory services, and abuse of delegated privileges within hybrid identity environments. Active Directory remains the primary identity store for the majority of enterprise environments, and directory infrastructure is implicated in the overwhelming majority of ransomware and breach events.

Semperis at 4.58% and Netwrix at 3.14% reflect this reality. Both vendors derive their ITDR revenue primarily from hybrid Active Directory and Entra ID threat detection – monitoring directory changes, detecting privilege escalation, and providing automated rollback of malicious modifications in ways that broader platform vendors do not replicate with the same depth or specialization. Their share reflects sustained enterprise demand for directory-specialist detection tools that sit alongside rather than inside larger security platforms. The coexistence of AD specialists with dominant platform vendors is a persistent structural feature of the ITDR market, driven by the fact that directory infrastructure requires dedicated monitoring approaches that general-purpose security platforms address incompletely.

Privileged access and NHI expansion are broadening the category

Another structural factor influencing share is the widening overlap between ITDR and adjacent identity categories. In earlier phases, ITDR was often framed around human account compromise and directory abuse. That framing is becoming too narrow. Modern environments increasingly require detection and response for privileged sessions, service accounts, workload identities, and AI agents operating with delegated authority. As a result, the operational boundary between ITDR, privileged access management, and non-human identity governance is becoming less distinct.

CyberArk, the third largest in the market, reflects this convergence directly. Many enterprises no longer view privileged access monitoring and identity threat detection as separate control problems. As attackers target both human and machine identities with equal sophistication, buyers increasingly want to detect anomalous behavior across the full spectrum of access pathways rather than only at the authentication layer. Silverfort’s 3.92% share reflects a related dynamic: its agentless architecture extends identity protection and behavioral detection across legacy systems and service accounts that sit outside the perimeter of modern identity platforms, covering a gap that larger vendors do not address without significant deployment complexity. BeyondTrust and Delinea similarly derive their ITDR share from privileged access-rooted detection, reflecting the growing enterprise preference for unified privileged access and threat detection over separate tool categories. This convergence should continue to support share for identity security incumbents as buyers prioritize control over the full identity attack surface – human, privileged, and machine – within a single operational framework.

Platform Convergence across the UADP Architecture

In the current market, the UADP opportunity can be approximated as the aggregate of the five underlying capability markets analyzed in this report: DSPM, DLP, AI security, NHI governance, and ITDR. Each of these markets developed independently and continues to generate revenue through distinct products and vendor ecosystems.

Looking forward, however, market expansion is unlikely to remain purely additive. As enterprise architectures evolve toward AI-driven workflows and automated infrastructure, buyers are increasingly prioritizing platforms capable of correlating signals across these domains. Data sensitivity, identity privileges, runtime behavior, and AI interactions must be evaluated together to produce effective security decisions. As a result, the long-term trajectory of the UADP market will depend not only on the growth of the underlying categories, but also on how effectively vendors integrate capabilities across these pillars into unified operational platforms.

This shift introduces an additional structural dimension to market growth: platform integration. Vendors that successfully assemble data security, identity governance, AI protection, and behavioral detection into a coherent control plane are likely to capture a disproportionate share of incremental spending. Conversely, vendors that remain confined to single-category products may find growth increasingly constrained as enterprise buyers favor integrated architectures capable of enforcing policy across complex AI-enabled workflows.

UADP Industry Analysis

The UADP market is projected to grow from $8.30B in 2025 to $21.59B in 2030, implying approximately 21.08% CAGR through 2030. Market size estimates are constructed by combining revenues from adjacent security segments, including DSPM, DLP, AI security, ITDR, and NHI security.The aggregated segment baseline serves as the foundation for UADP sizing in the near term, where spending remains distributed across distinct tools and buying centers. From this baseline, forward projections introduce a convergence adjustment to reflect the increasing consolidation of these capabilities into integrated platforms. This adjustment is applied at the market level to account for shifts in enterprise purchasing behavior, where multiple point solutions are replaced by unified architectures, reducing redundant spend across categories. As a result, the projected UADP market diverges from the simple sum of its components over time, with the 2030 estimate intentionally modeled below the aggregate total of the five segments.

The growth profile reflects both the expansion of the underlying security categories and the increasing demand for integrated security architectures capable of governing data, identities, and AI-driven workflows within a unified operational framework. Early adoption is driven by the rapid deployment of AI systems and the expansion of non-human identities, which are exposing gaps in traditional security controls. As vendors integrate capabilities across data security, identity governance, AI protection, and behavioral detection, the market transitions from independent category spending toward platform-based security investments, with convergence effects becoming more pronounced toward 2030.

Growth Drivers

Enterprise AI adoption is expanding the scope of data and identity governance

The rapid deployment of generative AI and autonomous agents across enterprise environments is expanding the scope of data governance beyond traditional storage systems. AI agents now retrieve enterprise knowledge, invoke APIs, and execute workflows with delegated authority, often interacting directly with sensitive data and internal systems. This evolution introduces new pathways through which data can be accessed, synthesized, or exposed during live execution. As organizations scale copilots, RAG systems, and agentic workflows, governance requirements increasingly extend to the entire interaction layer between users, agents, and enterprise data sources. Vendors are responding by integrating data security, identity governance, and runtime controls into unified platforms capable of monitoring how AI systems access and manipulate enterprise information.

Fragmentation across data, identity, and runtime security layers is creating demand for unified control planes

Most enterprise security architectures remain fragmented across multiple control layers. Data security platforms, identity governance systems, runtime protection tools, and threat detection solutions often operate independently and exchange limited context. As AI systems operate at machine speed and interact across multiple services simultaneously, these fragmented architectures struggle to provide real-time visibility and coordinated enforcement. Enterprises are therefore seeking platforms that can unify these signals into a shared policy and telemetry layer. The emerging UADP architecture reflects this shift, combining data protection, identity visibility, and runtime monitoring into a single security fabric designed to defend autonomous systems and the workflows they execute.

Autonomous agents are expanding the enterprise identity surface

AI systems increasingly operate with delegated privileges that allow them to access data, call external tools, and perform actions across enterprise applications. This creates a new category of non-human identities that must be governed alongside traditional user accounts. Unlike conventional software processes, AI agents can dynamically decide which resources to access or which actions to take based on contextual reasoning. As a result, security teams must monitor not only human activity but also the behavior of automated agents interacting with sensitive data and infrastructure. UADP platforms address this challenge by combining identity visibility, behavioral monitoring, and policy enforcement to control how both users and AI agents access enterprise systems.

AI systems introduce new runtime attack surfaces that traditional security models cannot address

Traditional security architectures were designed for deterministic software systems with predictable behavior. Agentic AI introduces probabilistic systems capable of generating new outputs, reasoning about tasks, and autonomously interacting with other services. These systems create new categories of risk, including prompt injection, unauthorized data retrieval, and agent-driven privilege escalation. Because these threats occur during the execution of AI workflows rather than at traditional network boundaries, they require security controls that operate directly within the runtime layer of AI applications. UADP platforms address this challenge by combining runtime protection, data governance, and threat detection capabilities to monitor and intervene in agentic workflows before sensitive data or systems are compromised.

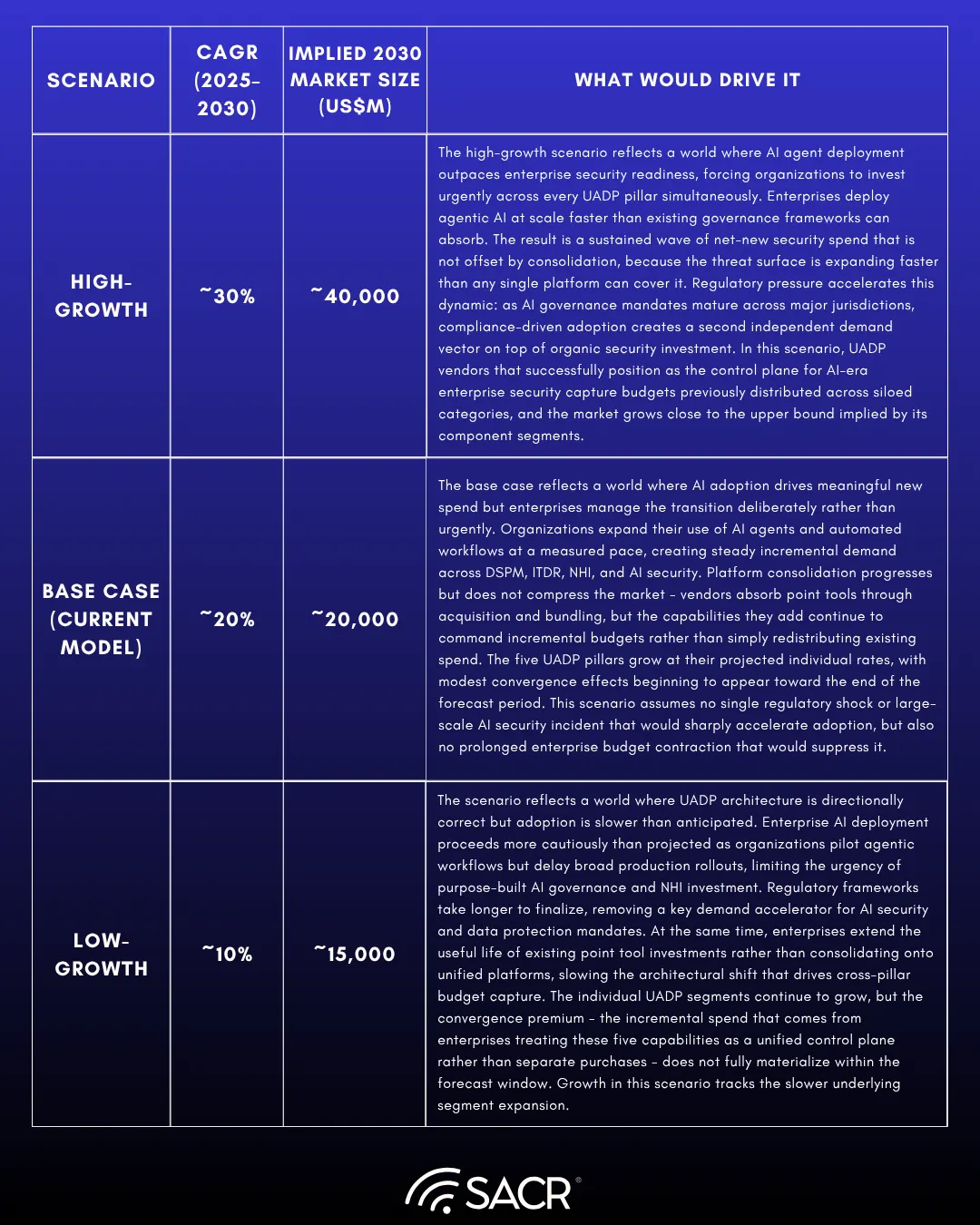

Scenario Analysis for UADP Market

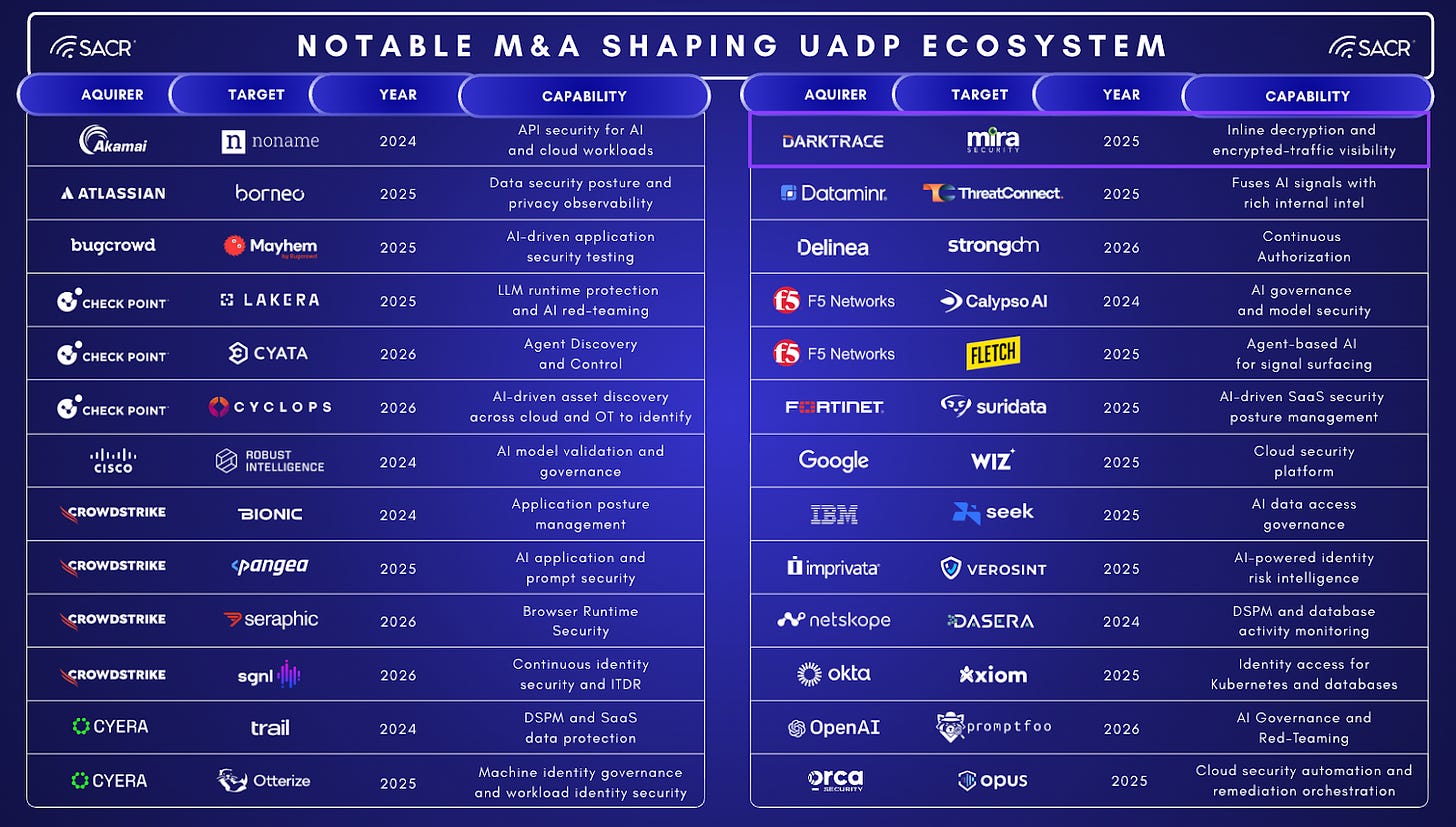

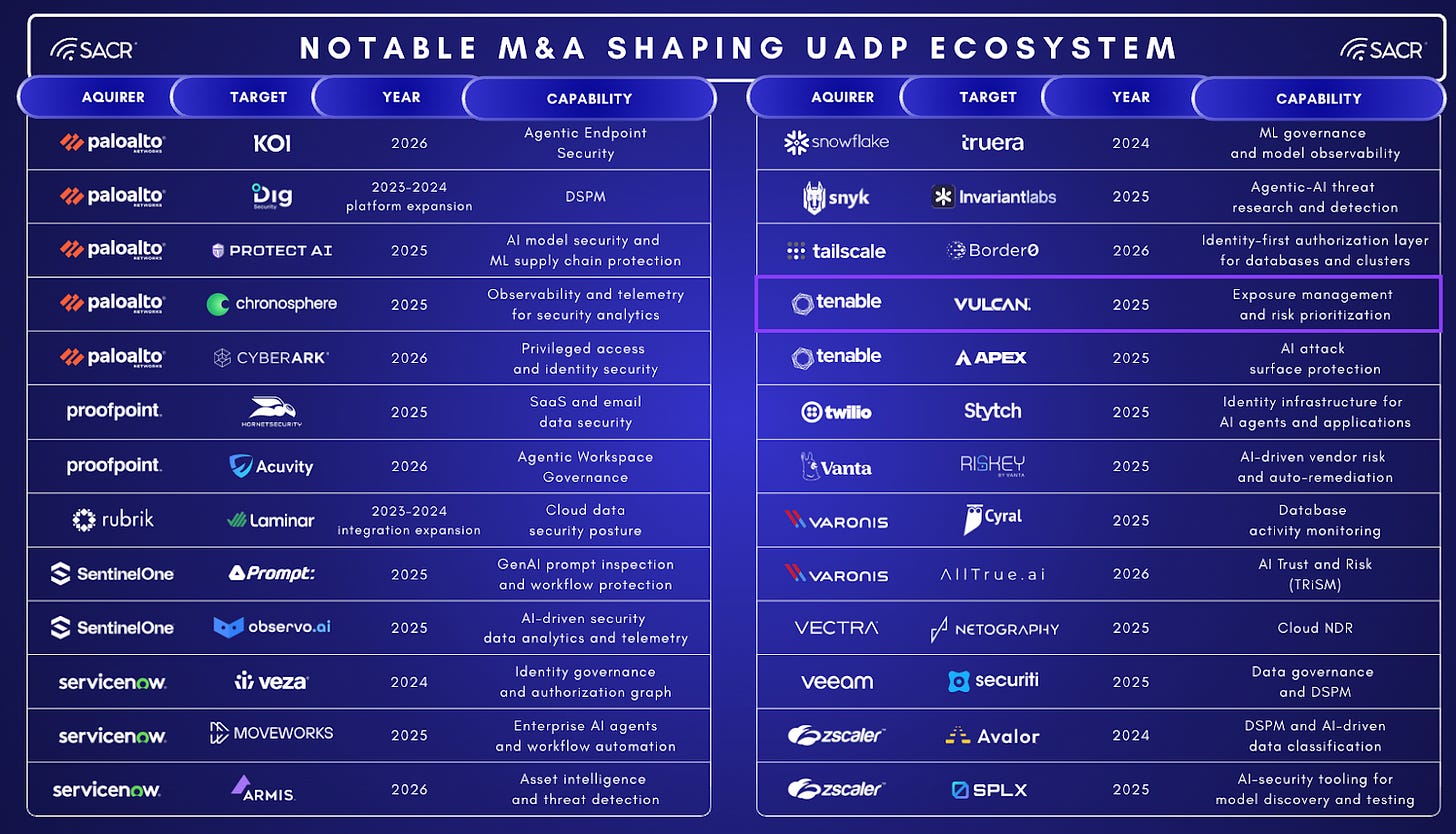

Notable M&A Shaping the UADP Ecosystem

Strategic acquisitions across the industry illustrate how vendors are assembling the capabilities required to compete in an integrated architecture.

Analysis of Key M&A

Palo Alto Networks → CyberArk (2026)

For Palo Alto, this acquisition resolves a structural gap that became increasingly difficult to defend as identity emerged as the primary attack surface in cloud and AI environments. Palo Alto’s platform had strong coverage across network, endpoint, and cloud infrastructure — but identity governance, privileged access, and machine identity management sat outside its control plane. CyberArk fills all three gaps simultaneously. The combined platform can now enforce security policy across users, privileged accounts, service accounts, and AI agent identities within a single architecture, eliminating the seam between infrastructure security and identity governance that attackers have increasingly exploited. The deal is significant because it demonstrates that the largest security platforms now treat identity not as an adjacent discipline but as a core enforcement layer – one that must be owned rather than integrated through partnership.

Google → Wiz (2025)

Google’s acquisition of Wiz is less about adding a capability and more about controlling the infrastructure layer where AI workloads, data pipelines, and enterprise applications increasingly run. Wiz’s risk graph connects cloud misconfigurations, workload vulnerabilities, and sensitive data exposure into a unified view, which is precisely the visibility foundation that any coherent security architecture requires before enforcement controls can operate effectively. Without knowing where sensitive data lives, which workloads have access to it, and what misconfigurations expose it, runtime controls and policy enforcement operate blind. The move signals that hyperscalers are not content to provide infrastructure and leave security to third parties. They intend to own the security control plane that sits on top of their infrastructure. For the broader market, this raises the competitive stakes for every vendor whose differentiation depends on cloud infrastructure visibility.

Veeam → Securiti AI (2025)

This deal is a directional signal about where resilience platforms must go to remain relevant. Backup and recovery vendors have historically operated after the fact — restoring systems once damage has occurred. But as AI systems begin interacting with large internal data stores, enterprises need to understand their sensitive data exposure before an incident, not after one. Securiti’s data governance and DSPM capabilities give Veeam the ability to identify what sensitive data exists, where it lives, and which AI workflows are touching it – converting a reactive recovery platform into a proactive data risk platform. The transaction reflects a broader pattern now visible across the security market: the data protection layer is attracting entrants from adjacent categories, including resilience, governance, and compliance, each of which is discovering that continuous data visibility has become a prerequisite for the products they already sell. Pure-play DSPM vendors face a market in which breadth expectations are rising not because buyers are demanding more features, but because the platforms surrounding them are absorbing the capability.

Cisco → Robust Intelligence (2024)

Cisco’s acquisition reflects a recognition that AI model security cannot be addressed solely through network controls or endpoint protection. It requires a dedicated layer that understands model behavior, adversarial inputs, and runtime integrity. What makes the deal strategically interesting is not the capability itself but what it reveals about where Cisco believes the enterprise security perimeter is moving. As large language models and agent-driven workflows become operational infrastructure, the attack surface shifts from network packets and endpoint processes toward prompts, tool calls, and model responses. Cisco is positioning to govern that surface before it becomes a default blind spot in enterprise security architectures, and the acquisition signals that traditional security vendors view AI model governance as a control problem that belongs inside the security stack rather than inside the AI development stack.

Check Point → Lakera (2025)

Check Point’s acquisition of Lakera targets the live interaction surface – the moment a prompt enters a model and a response leaves it. Lakera’s runtime protection detects prompt injection, jailbreak attempts, and adversarial inputs in real time, preventing models from being manipulated into exposing sensitive data or executing unintended actions. The distinction matters because AI runtime attacks are fundamentally different from traditional threats: they require no malware, no network intrusion, and no credential compromise, only a carefully constructed input. As enterprises embed copilots, AI assistants, and autonomous agents into production workflows, this attack surface grows proportionally with AI adoption rather than with infrastructure complexity, meaning it cannot be addressed through perimeter controls alone. Check Point’s move positions the company to govern model interactions directly within its broader security platform, defending a threat surface that most enterprise security architectures currently leave unaddressed.

UADP Convergence Wheel

Interpreting Vendor Positioning in a Converging Market

Because the UADP architecture emerges from the convergence of several previously independent security markets, traditional vendor market share analysis is less meaningful at the aggregate level than within the underlying pillars. Vendor revenue today often reflects legacy strength in a single domain such as DLP, identity governance, or threat detection rather than alignment with the integrated architecture described in this report. As a result, presenting a consolidated market share table for the combined UADP market would risk overstating vendors concentrated in mature categories while understating the strategic positioning of vendors assembling broader security platforms.

The competitive landscape is therefore better understood through a convergence framework that illustrates how vendors participate across the five foundational pillars examined in this report: DSPM, DLP, AI security, non-human identity governance, and identity threat detection and response. The UADP convergence wheel visualizes this ecosystem by positioning specialist vendors within individual capability domains while highlighting platforms that integrate signals across multiple pillars.

Vendor Ecosystem and Platform Positioning

The architecture organizes around three convergence zones that reflect how enterprise security problems are increasingly experienced in practice rather than how security budgets have historically been structured.

The Data Security zone encompasses both DSPM and DLP – the disciplines responsible for knowing where sensitive data lives and preventing it from moving in ways that violate policy. These capabilities are increasingly inseparable. Effective enforcement requires classification context, and classification without enforcement produces visibility without control. Vendors in this zone include both established platforms with deep enterprise distribution – Microsoft, Palo Alto, Broadcom, Zscaler – and a generation of cloud-native specialists such as Cyera, Varonis, BigID, and Cyberhaven that were built specifically for environments where data moves continuously across SaaS, cloud storage, and browser-mediated workflows. The presence of vendors like Wiz, Rubrik, and Veeam reflects the broader pattern of adjacent platforms entering data security from cloud infrastructure and resilience rather than from traditional DLP lineages.

The Identity Security zone encompasses both ITDR and NHI which are the disciplines responsible for detecting compromised identities and governing the machine and workload identities that now outnumber human users in most enterprise environments. These two capabilities are converging for the same reason that DSPM and DLP are converging: the threat surface no longer respects the boundary between them. Attackers that compromise a service account, abuse a delegated token, or hijack an AI agent’s credentials are simultaneously an ITDR problem and an NHI problem. Vendors in this zone reflect the full spectrum of identity security lineages. PAM-rooted platforms such as CyberArk, BeyondTrust, and Delinea; cloud identity incumbents such as Okta and Microsoft; detection-first platforms such as CrowdStrike, SentinelOne, and Semperis; and a newer generation of NHI specialists including Astrix, Oasis, Entro, and Veza that were built specifically for the machine identity problem before larger platforms moved to address it.

AI Security sits at the center of the architecture, not because it is the largest pillar by current revenue, but because it is the surface where data security and identity security intersect at the point of live model interaction. When an AI agent accesses a sensitive data store under delegated credentials, the risk cannot be evaluated by data controls or identity controls independently. It requires both simultaneously. The vendors positioned in the AI Security zone reflect the range of approaches the market is currently exploring: runtime protection platforms such as HiddenLayer and Lakera focused on prompt and model interaction defense; AI governance platforms such as Noma and WitnessAI focused on model lifecycle and agent behavior; and broader security platforms including Microsoft, Palo Alto, CrowdStrike, Zscaler, and Netskope that are extending existing enforcement architectures into AI interaction surfaces.

Structural Convergence Toward Integrated Platforms

Vendors that appear across multiple zones in the convergence wheel – Microsoft, Palo Alto, CrowdStrike, Zscaler, and Netskope – represent the current candidates for platform-level UADP ownership. Their presence across data security, identity security, and AI security is not incidental. Each has made deliberate moves through acquisition, product development, or platform extension to extend its control plane beyond its original domain. What distinguishes these platforms from specialists is not depth in any single pillar but the ability to correlate signals across pillars – connecting data sensitivity context to identity behavior to AI runtime activity in ways that single-domain vendors cannot replicate without significant integration work on the buyer’s part.

The vendors anchored within a single zone represent a different strategic position. Some hold deep capability in one pillar and are valued precisely for that specialization. Buyers with mature programs in identity governance or data classification often prefer purpose-built tools over platform coverage that is broad but shallow. Others are earlier-stage platforms whose long-term positioning depends on either expanding their own surface area before platform vendors close the capability gap or becoming acquisition targets as larger platforms race to fill holes in their architectures. Both outcomes are already visible in the transaction record. Palo Alto acquiring CyberArk, Google acquiring Wiz, CrowdStrike acquiring SGNL, and Cyera acquiring Otterize each reflect a platform vendor identifying a zone it did not adequately control and moving to own it through acquisition rather than organic development. The specialists that remain independent will increasingly be evaluated by buyers and by acquirers on the same question of whether their single-pillar depth justify a separate deployment, or if a multi-zone platform now covers the use case well enough.

Potential headwinds

The organizational ownership problem may slow platform consolidation

The UADP architecture assumes that enterprises will increasingly evaluate data security, identity governance, and AI risk as a unified control problem. In practice, these disciplines are owned by different teams with different budgets, different reporting lines, and different procurement cycles. Data security typically sits within compliance or data governance functions. Identity security is owned by IAM or infrastructure teams. AI risk governance, where it exists at all, is frequently split between security, legal, and the office of the CTO. In most enterprises, no single buyer owns all three simultaneously.

This organizational fragmentation creates a structural friction that architectural logic alone cannot overcome. A vendor assembling a unified UADP platform still needs a buyer willing to consolidate across these internal boundaries — and that buyer does not yet consistently exist. Enterprises may recognize the value of integrated control planes in the abstract while continuing to purchase capabilities through the teams and procurement channels that already exist. The result is that UADP adoption may proceed pillar by pillar through existing buying centers rather than as a unified platform purchase, slowing the consolidation dynamic that drives the convergence premium in the growth model. Until enterprises either create a dedicated function responsible for AI-era security architecture or until a sufficiently dominant platform forces consolidation from the outside, organizational structure remains a more durable headwind than any technology gap.

Hyperscaler absorption may compress the independent market

Hyperscalers hold a position in the UADP architecture that no independent security vendor can fully replicate – control over the infrastructure layer where AI workloads run, the identity plane through which access is granted, and the productivity environment where enterprise data is created and shared. Each of these positions is a potential absorption point for UADP capabilities that currently generate independent market revenue.

The Microsoft scenario is the most consequential. Defender, Purview, Entra, and the broader Microsoft security stack already span DLP, DSPM, ITDR, and NHI governance within a single licensing framework. If Microsoft continues to deepen these capabilities and bundle them within E5 or successor licensing tiers, a meaningful portion of the addressable UADP market could be captured through license expansion rather than through discrete security purchases. Enterprises that already rely on Microsoft for identity, productivity, and compliance infrastructure face a low-friction path to absorbing UADP capabilities without engaging the independent vendor market at all. Google’s acquisition of Wiz signals a similar intent at the cloud infrastructure layer, and AWS’s native IAM and secrets management capabilities already provide infrastructure-layer NHI coverage that reduces the urgency of standalone NHI purchases for AWS-centric environments. If hyperscaler platforms absorb the baseline UADP use case, the independent market may be structurally smaller than the segment aggregation implies – concentrated in high-maturity environments, complex multi-cloud architectures, and use cases that require depth the hyperscaler platforms do not provide.

Some enterprises may prioritize control layer specialization over platform consolidation

While platform convergence offers operational advantages, some organizations may prefer specialized tools that provide deeper functionality within individual security domains. For example, a company with a mature identity program may continue to rely on dedicated identity governance or privileged access management vendors even if UADP platforms offer overlapping capabilities. Similarly, organizations with complex data protection requirements may retain specialized tools for discovery, classification, or encryption.

This dynamic can lead to hybrid environments where unified platforms coexist with specialized systems rather than replacing them entirely. As a result, the UADP market may develop gradually through integration across existing security domains rather than through rapid platform consolidation.

Conclusion

Summary of Projections

The UADP market is projected to grow from $8.30 billion in 2025 to $21.59 billion by 2030, representing a 21.08% CAGR. That growth is real, but the more consequential question is structural: whether convergence produces an independent category or is absorbed into platforms that already control identity, data, and infrastructure.

The near-term trajectory is clear. Each of the five foundational pillars, DSPM, DLP, AI security, NHI governance, and ITDR, continues to expand as organizations respond to rising data exposure, the proliferation of machine identities, and the operational deployment of AI. Current market size reflects spending distributed across distinct tools and buying centers. The unresolved question is whether that spend consolidates into a unified architecture or is captured through platform expansion.

The competitive dynamic is not whether convergence occurs, but which vendor category defines it. Identity vendors hold a control-plane advantage at authentication and enforcement. Data security vendors hold a classification advantage through visibility into sensitive data. AI security vendors hold a runtime advantage through insight into model behavior and agent activity.

Vendors most likely to define the architecture are those that combine at least two of these advantages at scale. Microsoft integrates identity and data control across a platform already embedded in enterprise workflows, positioning it as the default control plane, though increasingly “good enough” bundling may cap differentiation. Palo Alto Networks is assembling the most credible independent platform, but its success depends on turning acquisitions into a coherent policy and enforcement layer. CrowdStrike is the strongest challenger, with a unified detection fabric across endpoint and identity, but remains weaker on the data control layer that anchors policy decisions.

Category Formation Is Not Guaranteed

The structural drivers supporting convergence are real, but category formation is not inevitable. There is a credible scenario in which UADP does not emerge as a distinct market and is instead absorbed into adjacent control planes.

Microsoft already bundles capabilities across DSPM, DLP, ITDR, and NHI within a unified licensing model. Hyperscalers control the infrastructure where AI workloads, data pipelines, and applications operate. If these platforms continue expanding native capabilities, a meaningful portion of demand will be captured through license expansion rather than standalone purchases.

In this scenario, the architectural logic of UADP holds, but the economic expression is compressed. Demand exists, but it accrues to platform vendors rather than forming a discrete category. The independent UADP market becomes concentrated in high-complexity, multi-cloud environments where platform-native capabilities are insufficient.

What to Watch

The most important developments over the next 12 to 18 months are organizational, not technological. The formation of unified security functions that consolidate ownership of identity, data, and AI risk under a single budget is the clearest indicator of market acceleration.

If that consolidation occurs, the convergence premium embedded in current projections is conservative. If enterprises continue to operate through fragmented buying centers, adoption will proceed incrementally and growth will track individual categories rather than a unified platform model. In that case, platform absorption becomes more likely regardless of architectural merit.

Strategic Implications

For vendors, the competitive question is no longer whether to integrate across pillars, but how quickly and through what mechanism. Organic expansion is increasingly insufficient given the pace of market consolidation. Recent activity, including Palo Alto Networks acquiring CyberArk, Google acquiring Wiz, and CrowdStrike acquiring SGNL and Seraphic, reflects the speed at which platforms are assembling cross-domain capabilities. Vendors that remain anchored in a single pillar face a narrowing window before adjacent capabilities are absorbed by larger platforms.

The strategic priority is to identify the highest-value adjacent domain that aligns with existing distribution and installed base, and to move into that domain before competitors close the gap. Identity security vendors are best positioned to expand into AI runtime governance, where access control and execution risk converge. Data security vendors must incorporate identity behavior context to move from visibility to enforcement. AI security vendors, in turn, need to anchor runtime protections in data classification and access policy frameworks. Vendors that delay expansion until the architecture stabilizes are likely to find that the most defensible positions have already been claimed.

For investors, the most important distinction is between genuine architectural integration and portfolio aggregation. Multi-pillar positioning alone is not sufficient. Prior transitions such as XDR and CNAPP demonstrated that valuation premiums ultimately accrue to vendors that deliver unified detection and enforcement, rather than those that simply assemble adjacent products. The same dynamic is likely to apply in UADP. Vendors where cross-domain signal correlation is already visible, where identity risk informs data access decisions or AI runtime violations feed back into identity controls, are more likely to sustain long-term platform value.

Conversely, vendors that present a broad portfolio but continue to operate each pillar independently represent integration risk rather than platform premium. In these cases, the absence of a unified control layer limits both differentiation and defensibility. On the specialist side, the highest-value acquisition targets are vendors in AI security and NHI governance that combine deep technical differentiation with limited distribution. These vendors are difficult to replicate organically and can be scaled effectively through an acquirer’s existing enterprise relationships.

For enterprise security leaders, the immediate priority is not platform selection but organizational alignment. The primary constraint on UADP adoption is not the availability of technology, but the fragmentation of ownership across data security, identity governance, and AI risk functions. As long as these domains operate under separate budgets, tools, and reporting structures, the value of unified control planes cannot be fully realized.

Security leaders should begin by identifying where policy decisions require coordination across teams. These coordination points represent the clearest opportunities for consolidation and the most immediate sources of operational efficiency. In parallel, AI governance must be treated as an operational security discipline rather than a compliance exercise. The runtime risks introduced by autonomous systems are already present, and delaying implementation of controls until standards mature introduces avoidable exposure during the period of fastest adoption.